Marriott International Reports Fourth Quarter and Full Year 2025 Results

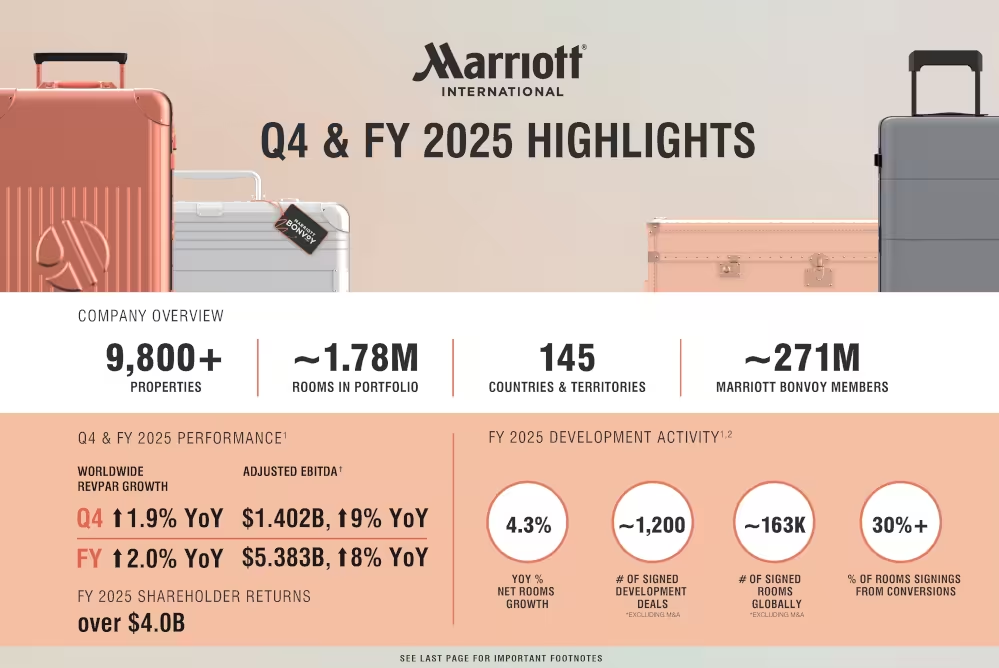

Marriott International, Inc.reported fourth quarter and full year 2025 results. RevPAR: - Q4: +1.9% worldwide (International +6.1%, U.S. & Canada –0.1%). - Full Year: +2.0% worldwide (International +5.1%, U.S. & Canada +0.7%). Earnings: - Q4 Net Income: $445M (Adjusted $695M). - FY Net Income: $2.6B (Adjusted $2.74B). - Q4 Adjusted EPS: $2.58; FY Adjusted EPS: $10.02. EBITDA: - Q4 Adjusted EBITDA: $1.4B (+9% YoY). - FY Adjusted EBITDA: $5.38B. Rooms Growth: ~100,000 gross rooms added in 2025; net growth +4.3%. Pipeline: Record 4,100 properties (~610,000 rooms), 43% under construction. Shareholder Returns: $4.0B returned via dividends and buybacks. Operational Highlights - Luxury Outperformance: Global luxury RevPAR rose >6% in Q4. - Development Momentum: 163,000 organic rooms signed in 2025; ~⅓ from conversions. - Portfolio Expansion: - Integrated citizenM (37 hotels, 8,800 rooms). - Launched Series by Marriott™ in India, U.S., and Canada. - Loyalty Strength: - Added 43M new Bonvoy members (total ~271M). - Member stays accounted for 75% of U.S./Canada room nights, 68% globally. Balance Sheet - Debt: $16.2B (up from $14.4B in 2024). - Cash: $0.4B. - Share Repurchases: 12.1M shares ($3.3B) in 2025. 2026 Outlook - RevPAR growth: +1.5–2.5%. - Net rooms growth: +4.5–5%. - Adjusted EBITDA growth: +8–10%. - Capital returns: >$4.3B expected. Marriott’s results show steady global growth, with international markets (especially EMEA and Asia Pacific) driving performance, while U.S. & Canada remained flat due to business travel softness. The company’s asset-light model, loyalty strength, and aggressive pipeline position it for continued expansion.

Follow us on Insta