Marriott International Reports First Quarter 2026 Results

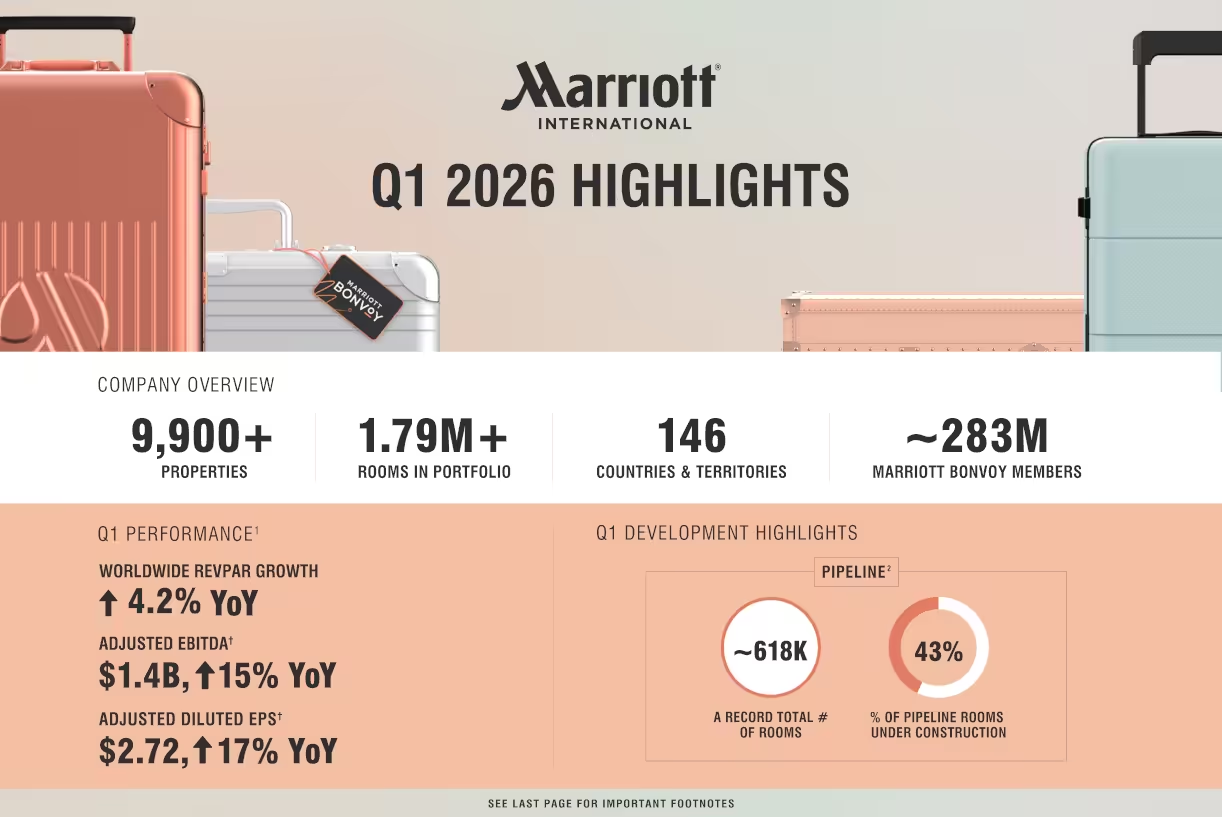

Marriott International, Inc. reported first quarter 2026 results. Financial Performance - RevPAR (Revenue per Available Room): Up 4.2% worldwide, with 4.0% growth in U.S. & Canada and 4.6% internationally. - Net Income: Reported at $648M (down 3% YoY); Adjusted net income $726M (up from $645M in Q1 2025). - EPS: Reported diluted EPS $2.43; Adjusted diluted EPS $2.72 (vs. $2.32 last year). - Adjusted EBITDA: $1.398B, a 15% increase YoY. Growth & Development - Added 15,900 net rooms globally in Q1, with ~7,500 in international markets. - Global system now totals 9,900+ properties and nearly 1.8M rooms. - Development pipeline reached a record 4,107 properties / 618,000 rooms, with 43% under construction. - Conversions remain strong, representing 35% of signings and 40% of openings. Regional Trends - APEC: RevPAR up 7%, driven by leisure demand. - Greater China: RevPAR up nearly 6%, especially in Hong Kong & Hainan. - EMEA: RevPAR up 3%, though Middle East performance was impacted by regional conflict. Loyalty & Platform - Marriott Bonvoy membership grew to 283M members. - Bonvoy continues to be a major driver of customer engagement and owner value. Shareholder Returns - Repurchased 2.1M shares for $0.7B in Q1; year-to-date returns to shareholders exceed $1.2B (dividends + buybacks). - Issued $1.45B in senior notes due 2033 and 2038. Outlook - Company expects continued impact from Middle East conflict through 2026. - Pipeline momentum and Bonvoy loyalty platform seen as key growth drivers. - Plans include a U.S. hotel sale (with impairment charge) and an investment in Lefay Resorts later in 2026. Marriott’s Q1 2026 results show steady global demand recovery, strong pipeline growth, and loyalty expansion, even amid geopolitical challenges.

Follow us on Insta