Qantas Group Reported solid financial performance for the first half of FY2026

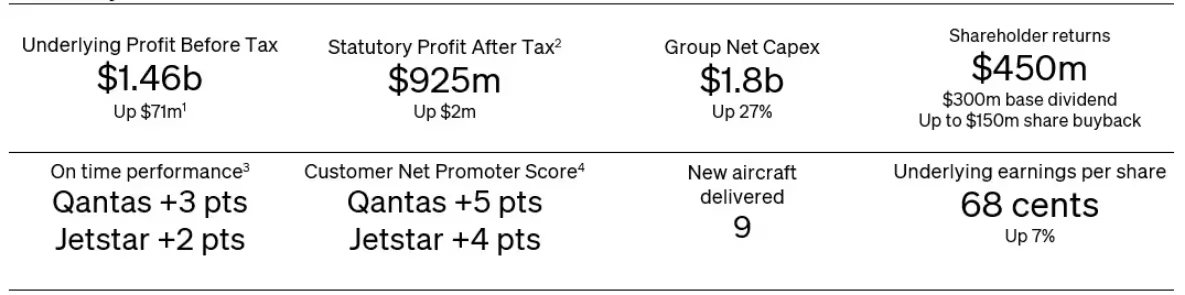

Qantas Group ended the half with $12.6 billion of liquidity, including $1.8 billion in cash, $1.2 billion in committed undrawn facilities and $9.6 billion in unencumbered fleet and other assets. Liquidity: $12.6 billion - $1.8 billion in cash - $1.2 billion in undrawn facilities - $9.6 billion in unencumbered fleet & assets Net Debt: $5.6 billion (bottom of target range $5.6–$7.0 billion) Capital Expenditure: - $1.8 billion in 1H26 (fleet renewal acceleration) - FY26 forecast: $4.1–$4.3 billion - FY27 forecast: $5.1–$5.4 billion Shareholder Returns - Dividend: Fully franked interim base dividend of $300 million (19.8 cents/share) - 20% increase vs. 1H25 and 2H25 - Payment date: 15 April 2026 - Buyback: On-market share buyback up to $150 million Outlook & Key Assumptions - Demand: Strong travel demand expected across portfolio - Revenue Guidance: - Domestic unit revenue: +3% YoY in 2H26 - International unit revenue: +1–3% YoY in 2H26 - Qantas Loyalty: Underlying EBIT growth of 10–12% in FY26 Cost & Transformation - Fleet Transition Costs: ~$160 million in FY26 (A321XLR introduction) - Same Job Same Pay: ~$95 million gross impact in FY26 - Restructuring Charges: ~$110 million in 2H26 (Jetstar Asia closure + restructuring) - Fuel Costs: ~$2.5 billion in 2H26 (hedging + carbon costs, $35m transformation benefit) - Depreciation/Amortisation: ~$2.25 billion in FY26 - Net Finance Costs: ~$300 million - Transformation Target: ~$400 million in FY26 (offsetting CPI, 40% in 1H26, 60% in 2H26) Strategic Commitment - Net debt expected to remain at or below mid-range of target. - Management reaffirmed margin targets for airline businesses and EBIT targets for Qantas Loyalty. This paints a picture of Qantas balancing fleet renewal investment, shareholder returns, and transformation initiatives while maintaining strong liquidity and demand outlook.

Follow us on Insta